|

What do Internal Auditors do?

Internal Audit is a multidimensional discipline that spans over all sectors that has evolved to a key position within organisations. The internal auditor is often described as the organisation’s critical friend – the independent advisor who can challenge current practice, champion best practice and be a catalyst for improvement with the objective of ensuring that the organisation as a whole can achieve its strategic objectives. As advisors to management, Internal Auditors act as the right hand of the Board of Directors through the Audit Committee by giving assurance on the organisations ability to meet its objectives, its governance, risks and controls. Internal Auditors often have input into strategic planning, market analysis, compliance, change management and the use of information technology.

Although Internal Audit does have a degree of focus on the financial aspects of the organisation, it is essentially not a financial discipline – unlike its counterpart External Audit. Its multidimensional nature mandates a much broader scope in the organisation than that of External Audit. The nature of the Internal Auditor’s daily work creates the opportunity to acquire a significant amount of depth and breadth of understanding of the organisation’s strategy and operations. Its multidimensional nature therefore inevitably shapes internal auditors into ideal candidates for executive positions.

|

|

Role of Internal Audit

Internal Auditors are responsible for the following:

|

| |

Evaluating controls and advising managers at all levels

- The Internal Auditor’s work includes assessing the tone and risk management culture of the organisation as well as evaluating and reporting on the effectiveness and efficiency of the implementation of management policies.

Evaluating risks

- Internal Auditors identify key activities and relevant risk factors and assess their significance. Changing trends and business/economic conditions impact the way the internal auditor assesses risk. The techniques of internal auditing have changed from a reactive and control based form to a more proactive and risk based approach. This enables the internal auditor to anticipate possible future concerns and opportunities as well as identifying current issues.

Analysing operations and confirming information

- Internal Auditors work closely with line managers to review operations then report their findings. The internal auditor must be well versed in the strategic objectives of the organisation, so that they have a clear understanding of how the operations of any given part of the organisation fit into the bigger picture.

Reviewing compliance

- Compliance review ensures that the organisation is adhering to rules, regulations, laws, codes of practice, guidelines and principles as they apply individually and collectively to all parts of their organisation

|

|

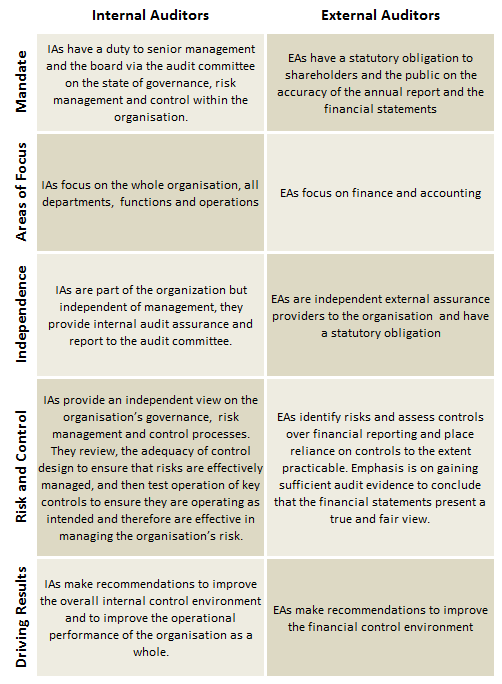

Differences between Internal Auditors (IAs) and External Auditors (EAs)

Although Internal Audit does have a degree of focus on the financial aspects of the organisation, it is essentially not a financial discipline - unlike its counterpart External Audit. Its multidimensional nature mandates a much broader scope in the organisation than that of External Audit.

|

|

|